Fillable Promissory Note Template

Fillable Promissory Note Template

Incomplete Information: Failing to fill in all required fields can lead to confusion and disputes later. Ensure every section is addressed.

Incorrect Amount: Double-check the loan amount. Errors in this figure can result in significant financial implications.

Missing Signatures: Both the borrower and lender must sign the document. Without signatures, the note may not be legally binding.

Improper Dates: Ensure the date of the agreement is accurate. An incorrect date can complicate the enforcement of the note.

Ambiguous Terms: Clearly define the repayment terms, including interest rates and payment schedules. Vague language can lead to misunderstandings.

Ignoring State Laws: Each state has specific requirements for promissory notes. Familiarize yourself with these to avoid legal issues.

Neglecting to Include Default Terms: Specify what happens in case of default. This can protect both parties and clarify expectations.

Not Keeping Copies: Failing to retain copies of the signed note can create problems if disputes arise. Always keep a record.

Overlooking Witnesses or Notarization: Depending on the state, having a witness or notarization may be necessary for the note's validity.

When filling out the Promissory Note form, it is important to follow certain guidelines to ensure accuracy and legality. Below are five things you should do and five things you should avoid.

Things You Should Do:

Things You Shouldn't Do:

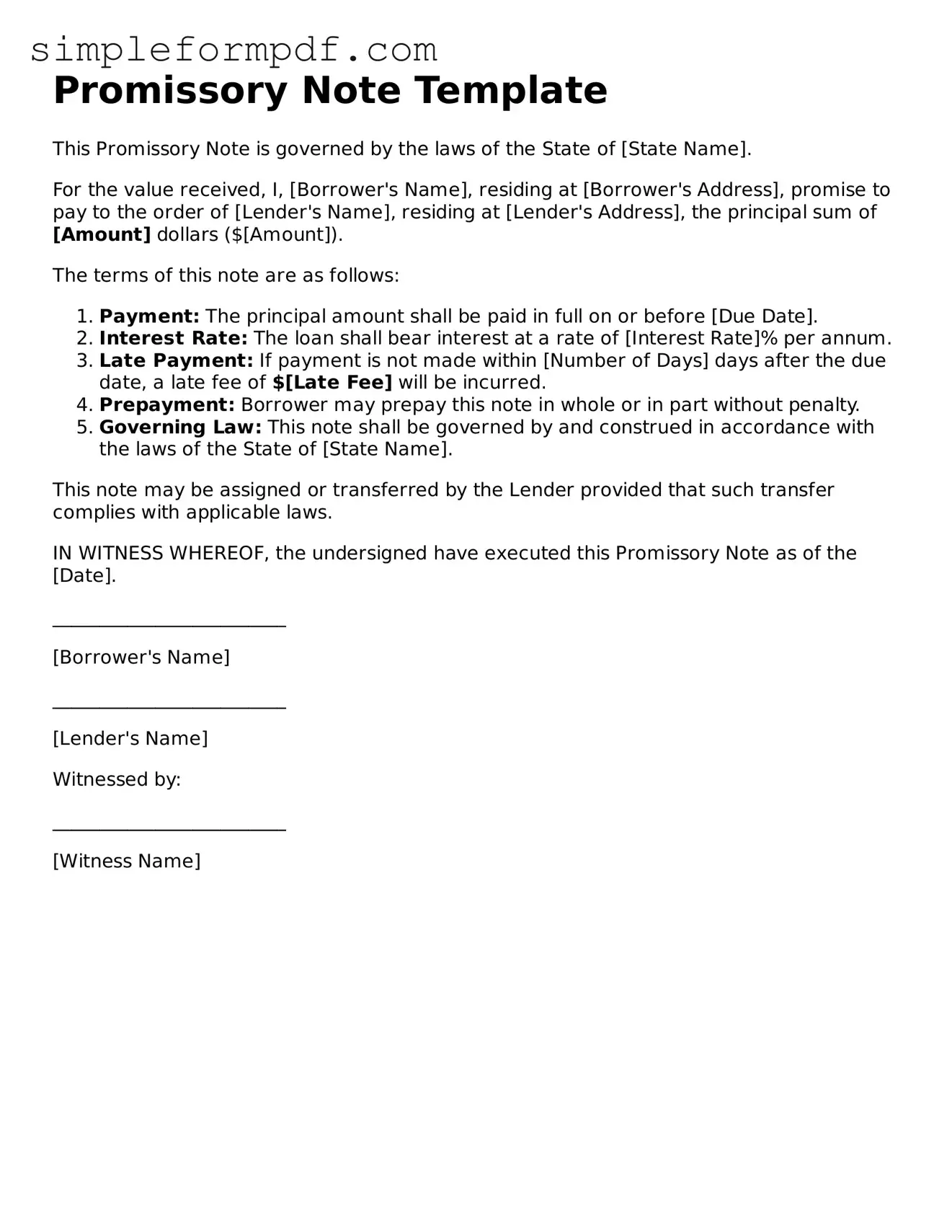

Promissory Note Template

This Promissory Note is governed by the laws of the State of [State Name].

For the value received, I, [Borrower's Name], residing at [Borrower's Address], promise to pay to the order of [Lender's Name], residing at [Lender's Address], the principal sum of [Amount] dollars ($[Amount]).

The terms of this note are as follows:

This note may be assigned or transferred by the Lender provided that such transfer complies with applicable laws.

IN WITNESS WHEREOF, the undersigned have executed this Promissory Note as of the [Date].

_________________________

[Borrower's Name]

_________________________

[Lender's Name]

Witnessed by:

_________________________

[Witness Name]

Broward Animal Care and Adoption - Pet owners should keep a copy of this form for their records and in case of emergencies.

The helpful guide to the Mobile Home Bill of Sale form is necessary for anyone looking to formalize the sale of a mobile home in Florida. This document not only serves as a receipt but also establishes clear ownership transfer, ensuring that both buyers and sellers understand their rights and obligations.

Loi Meaning in Job - Encourages candidates to prepare for future discussions.

Understanding promissory notes is crucial for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Here are five common misconceptions about the promissory note form:

Addressing these misconceptions can help individuals navigate the complexities of promissory notes more effectively.

Completing a Promissory Note form is an essential step in formalizing a loan agreement. It serves as a written promise to repay borrowed money under specified terms. Once you have gathered the necessary information, you can proceed to fill out the form accurately to ensure clarity and enforceability.

After completing the form, ensure that both parties retain a signed copy for their records. This will provide a clear reference in the event of any disputes or misunderstandings in the future.