Free Promissory Note Form for the State of New Jersey

Free Promissory Note Form for the State of New Jersey

Missing Borrower Information: Failing to include the full name and address of the borrower can lead to confusion later. Always ensure this information is accurate and complete.

Incorrect Lender Information: Just like with the borrower, the lender’s name and address must be correct. Double-check spelling and details.

Not Specifying the Loan Amount: Clearly state the exact amount being borrowed. Ambiguity can create disputes.

Ignoring Interest Rate Details: If the loan has an interest rate, it should be clearly defined. Forgetting this can lead to misunderstandings.

Omitting Payment Schedule: Specify when payments are due and how they will be made. This includes the frequency of payments and the final due date.

Not Including Late Fees: If there are penalties for late payments, these should be clearly stated. This protects the lender's interests.

Failing to Sign and Date: The document must be signed and dated by both parties. A missing signature can invalidate the agreement.

Not Initialing Changes: If any modifications are made to the form, both parties should initial these changes to acknowledge agreement.

Using Ambiguous Language: Be clear and precise in wording. Avoid terms that could be interpreted in multiple ways.

Neglecting to Keep Copies: Always keep a signed copy of the promissory note for your records. This is essential for future reference.

Loan Agreement: Similar to a promissory note, a loan agreement outlines the terms of a loan, including the amount borrowed, interest rate, and repayment schedule. It provides a comprehensive framework for the lender and borrower.

Mortgage: A mortgage is a specific type of loan agreement secured by real property. It details the borrower's obligation to repay the loan and the lender's rights in the event of default.

Security Agreement: This document establishes a security interest in personal property as collateral for a loan. Like a promissory note, it specifies the obligations of the borrower.

Installment Agreement: An installment agreement allows for the repayment of a debt in regular, scheduled payments. It shares similarities with a promissory note in terms of outlining payment terms.

Personal Guarantee: A personal guarantee is a promise made by an individual to repay a loan if the primary borrower defaults. It often accompanies a promissory note to provide additional security for the lender.

Letter of Credit: A letter of credit is a financial document issued by a bank guaranteeing payment to a seller on behalf of a buyer. It can be similar in function to a promissory note as it represents a promise to pay.

Debt Acknowledgment: This document confirms that a borrower acknowledges a debt owed to a lender. It serves as a formal recognition of the obligation similar to a promissory note.

Bond: A bond is a formal contract to repay borrowed money with interest at specified intervals. Like a promissory note, it represents a promise to pay back the principal amount.

Residential Lease Agreement: This document defines the relationship between a landlord and tenant, outlining essential terms such as rent, duration, and maintenance responsibilities. For more details, you can refer to azformsonline.com/residential-lease-agreement/.

Lease Agreement: In certain contexts, a lease agreement can function similarly to a promissory note, especially when it includes payment terms for rent, which the lessee must adhere to.

Credit Agreement: This document outlines the terms of a credit arrangement between a lender and a borrower. It shares features with a promissory note by specifying repayment obligations and conditions.

When filling out the New Jersey Promissory Note form, it's essential to approach the process with care. Here’s a helpful list of things to do and avoid:

By following these guidelines, you can ensure that your Promissory Note is correctly completed and legally binding.

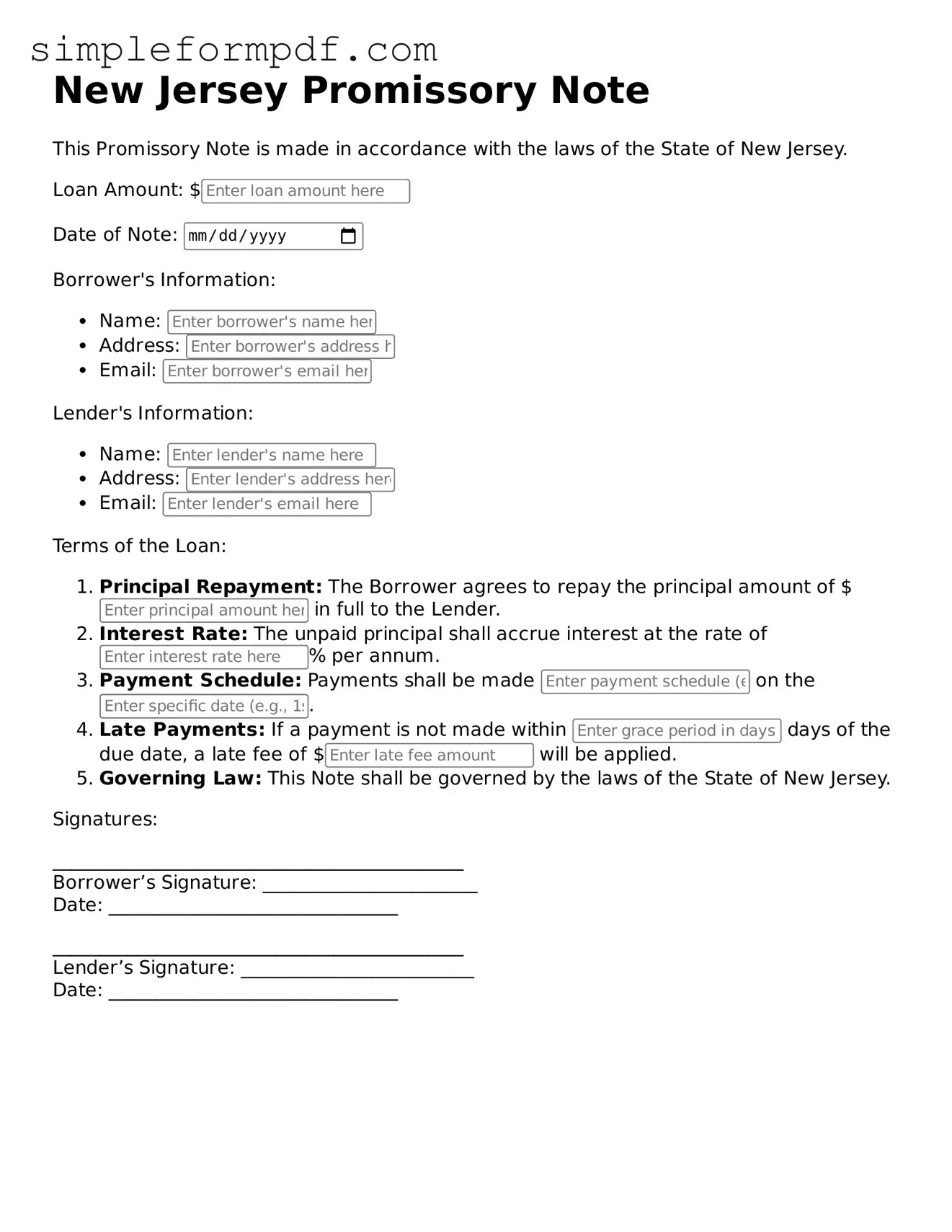

New Jersey Promissory Note

This Promissory Note is made in accordance with the laws of the State of New Jersey.

Loan Amount: $

Date of Note:

Borrower's Information:

Lender's Information:

Terms of the Loan:

Signatures:

____________________________________________

Borrower’s Signature: _______________________

Date: _______________________________

____________________________________________

Lender’s Signature: _________________________

Date: _______________________________

Pennsylvania Promissory Note - Having a witness sign the promissory note can provide additional validation of the agreement.

Loan Promissory Note - The form also provides transparency about the loan terms, helping to prevent misunderstandings.

California Promissory Note Requirements - Clear identification of all parties involved helps establish accountability in the agreement.

The reinstatement process for nursing licenses in Georgia can be complex, but the georgiaform.com/ provides essential resources to help navigate the necessary steps and requirements, ensuring that applicants are well-prepared to meet the state's standards for returning to their vital roles in healthcare.

Promissory Note Texas - It typically includes important details such as the loan amount, interest rate, and payment frequency.

Understanding the New Jersey Promissory Note form is essential for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Here are nine common misconceptions about this form:

Being aware of these misconceptions can help individuals navigate the complexities of promissory notes in New Jersey effectively.

Once you have the New Jersey Promissory Note form ready, you will need to fill it out carefully to ensure all necessary information is provided. After completing the form, it should be signed and dated by the involved parties to make it legally binding.