Free Promissory Note Form for the State of Illinois

Free Promissory Note Form for the State of Illinois

Incorrect Names: One common mistake is not using the full legal names of the borrower and lender. Abbreviations or nicknames can lead to confusion and complications.

Missing Signatures: Failing to sign the document is a frequent oversight. Both parties must sign the note for it to be valid.

Improper Dates: Some people forget to include the date of the agreement. Without a date, it can be challenging to determine the timeline of payments.

Unclear Payment Terms: Vague terms regarding payment amounts and schedules can lead to misunderstandings. Clearly stating these details is crucial for both parties.

When filling out the Illinois Promissory Note form, it is important to follow certain guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do.

Following these guidelines can help ensure that your Promissory Note is valid and enforceable. Careful attention to detail is crucial in this process.

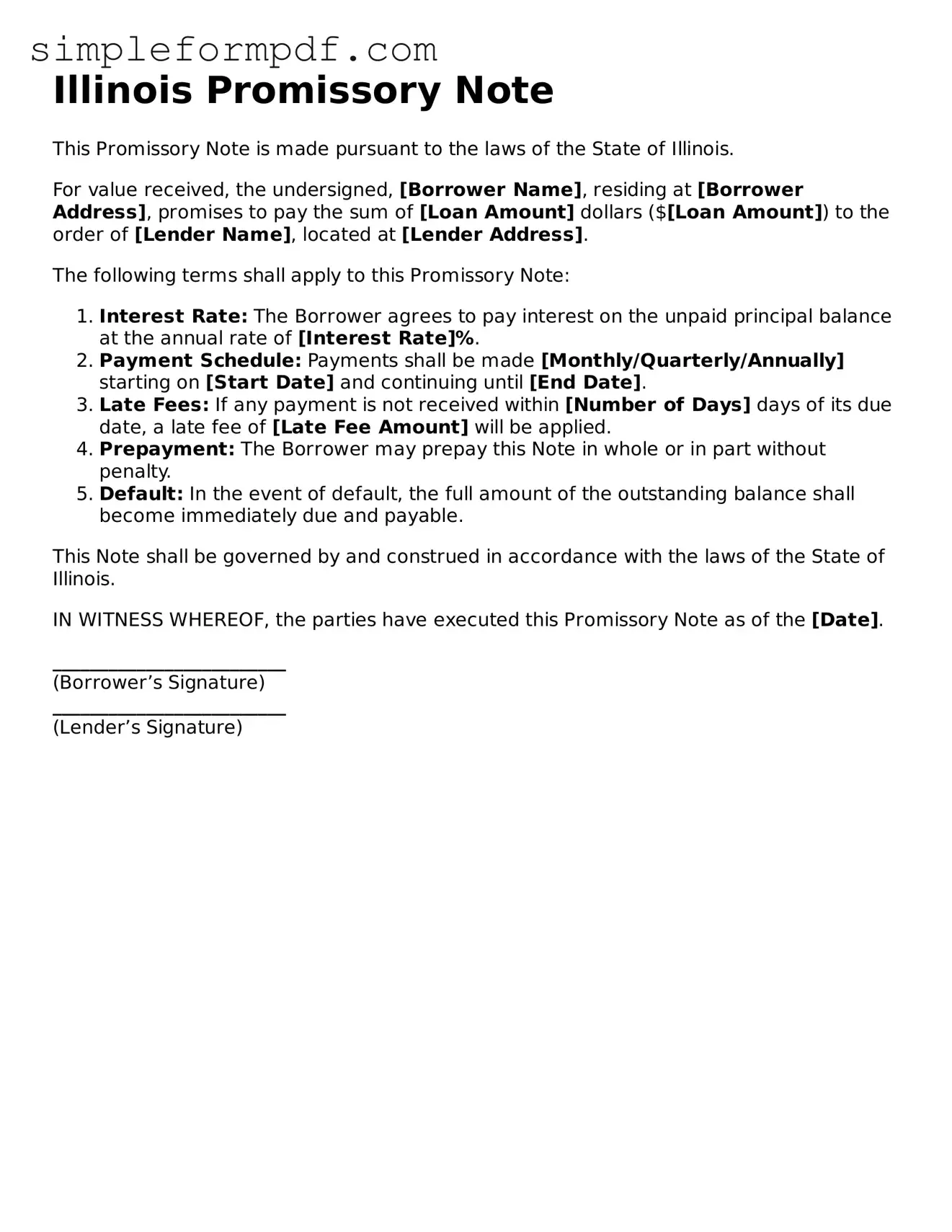

Illinois Promissory Note

This Promissory Note is made pursuant to the laws of the State of Illinois.

For value received, the undersigned, [Borrower Name], residing at [Borrower Address], promises to pay the sum of [Loan Amount] dollars ($[Loan Amount]) to the order of [Lender Name], located at [Lender Address].

The following terms shall apply to this Promissory Note:

This Note shall be governed by and construed in accordance with the laws of the State of Illinois.

IN WITNESS WHEREOF, the parties have executed this Promissory Note as of the [Date].

_________________________

(Borrower’s Signature)

_________________________

(Lender’s Signature)

How to Create Promissory Note - Many financial institutions favor promissory notes for formalizing loans.

The Arizona Homeschool Letter of Intent is a crucial document that parents must submit to officially notify the state of their decision to homeschool their children. This form serves as a formal declaration of intent, ensuring compliance with Arizona's educational regulations. Understanding its requirements and process is essential for a smooth homeschooling experience. For more information, you can visit https://azformsonline.com/homeschool-letter-of-intent.

Washington Promissory Note - A properly executed Promissory Note helps facilitate trust between parties.

When it comes to the Illinois Promissory Note form, there are several misconceptions that can lead to confusion. Understanding these can help ensure that you use the form correctly and avoid potential pitfalls. Here are seven common misconceptions:

By understanding these misconceptions, you can navigate the world of promissory notes with greater confidence. Always consider consulting with a legal professional if you have questions or concerns regarding your specific situation.

Once you have the Illinois Promissory Note form in hand, it’s time to fill it out accurately. This document will serve as a written promise to repay a loan, outlining the terms agreed upon by both parties. Follow these steps to ensure you complete the form correctly.

After completing the form, keep copies for both parties. This ensures everyone has a record of the agreement. If needed, consult with a legal professional to confirm that all details are correct and enforceable.