Free Loan Agreement Form for the State of Illinois

Free Loan Agreement Form for the State of Illinois

Incomplete Information: One of the most common mistakes is leaving sections blank. Every part of the form must be filled out completely. Omitting information can delay processing or lead to misunderstandings.

Incorrect Dates: Failing to provide accurate dates can create confusion. Ensure that the start and end dates of the loan are clearly stated and correctly formatted.

Wrong Loan Amount: Entering an incorrect loan amount can have serious implications. Double-check the figures to ensure they match the agreed-upon terms.

Missing Signatures: A common oversight is forgetting to sign the document. Both parties must provide their signatures to validate the agreement.

Failure to Read Terms: Skimming through the terms and conditions can lead to unexpected obligations. Take the time to read and understand the entire agreement before signing.

Not Keeping a Copy: After filling out the form, some individuals neglect to keep a copy for their records. Always retain a signed copy for future reference.

When considering a Loan Agreement, it's helpful to understand how it relates to other financial documents. Here are eight documents that share similarities with a Loan Agreement:

Non-disclosure Agreement: A Missouri Non-disclosure Agreement (NDA) is a legal document designed to protect sensitive information shared between parties. By establishing clear boundaries regarding confidentiality, this form helps safeguard trade secrets and proprietary data. If you need to secure your business interests, consider filling out the NDA form by clicking the button below: Missouri PDF Forms.

When filling out the Illinois Loan Agreement form, it’s important to approach the task with care. Here’s a list of things you should and shouldn’t do to ensure that your agreement is clear and legally binding.

By following these guidelines, you can help ensure that your Illinois Loan Agreement is filled out correctly and meets all necessary requirements.

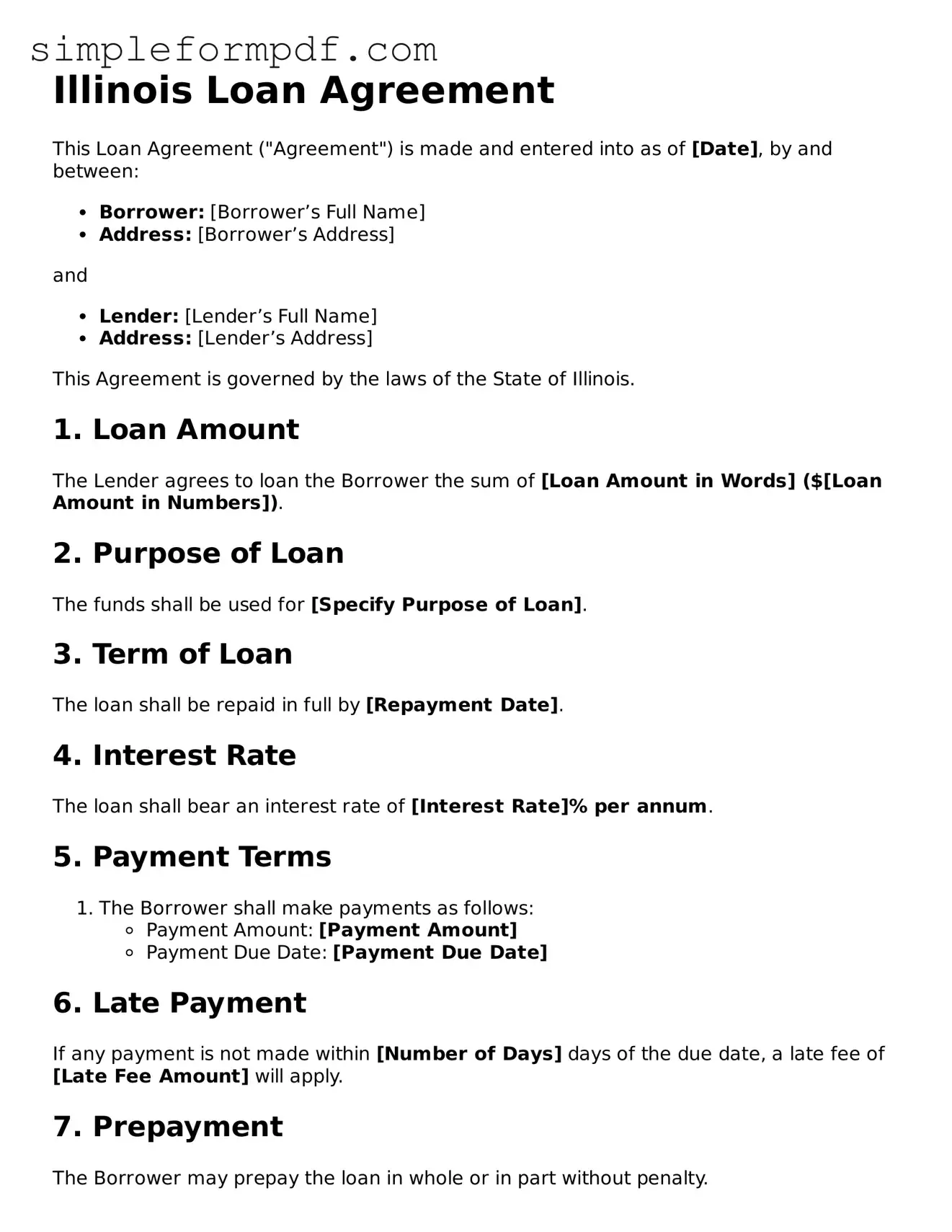

Illinois Loan Agreement

This Loan Agreement ("Agreement") is made and entered into as of [Date], by and between:

and

This Agreement is governed by the laws of the State of Illinois.

1. Loan Amount

The Lender agrees to loan the Borrower the sum of [Loan Amount in Words] ($[Loan Amount in Numbers]).

2. Purpose of Loan

The funds shall be used for [Specify Purpose of Loan].

3. Term of Loan

The loan shall be repaid in full by [Repayment Date].

4. Interest Rate

The loan shall bear an interest rate of [Interest Rate]% per annum.

5. Payment Terms

6. Late Payment

If any payment is not made within [Number of Days] days of the due date, a late fee of [Late Fee Amount] will apply.

7. Prepayment

The Borrower may prepay the loan in whole or in part without penalty.

8. Default

If the Borrower fails to make a payment or violates any terms of this Agreement, the Lender has the right to demand full repayment of the outstanding balance.

9. Governing Law

This Agreement shall be governed by and construed in accordance with the laws of the state of Illinois.

10. Signatures

By signing below, both parties agree to the terms of this Loan Agreement.

Free Promissory Note Template Texas - Outlines circumstances under which the lender may charge late fees.

Promissory Note New York - The agreement includes interest rates and any fees associated with the loan.

For those looking to navigate the process of purchasing a golf cart, understanding the Florida Golf Cart Bill of Sale requirements is essential. This document plays a critical role in the transaction, ensuring all legal aspects are addressed. You can find more information on how to properly complete and utilize this form by visiting these important guidelines on Golf Cart Bill of Sale paperwork.

Promissory Note Template Florida - They can be used for both secured and unsecured loans.

Understanding the Illinois Loan Agreement form is crucial for both lenders and borrowers. However, several misconceptions can lead to confusion. Below is a list of common misunderstandings regarding this important legal document.

By addressing these misconceptions, both lenders and borrowers can approach the Illinois Loan Agreement form with a clearer understanding and greater confidence.

Completing the Illinois Loan Agreement form is a straightforward process that requires careful attention to detail. Once you have gathered the necessary information, you can proceed with filling out the form accurately to ensure it meets legal requirements.