Free Deed in Lieu of Foreclosure Form for the State of Illinois

Free Deed in Lieu of Foreclosure Form for the State of Illinois

Failing to provide accurate property information. When filling out the form, individuals often overlook the necessity of including the correct legal description of the property. This description should be precise and match what is recorded in public records.

Not including all required signatures. It is essential that all parties involved in the property ownership sign the deed. Omitting a signature can lead to complications and may render the deed invalid.

Neglecting to notarize the document. The deed must be notarized to ensure its authenticity. Without notarization, the document may not be recognized by lenders or courts.

Incorrectly identifying the grantee. The grantee is the party receiving the property. Errors in naming the grantee can result in legal disputes and may delay the process.

Overlooking tax implications. Many individuals do not consider the potential tax consequences of a deed in lieu of foreclosure. It is advisable to consult a tax professional to understand any liabilities that may arise.

Failing to communicate with the lender. Before completing the deed, it is crucial to discuss the process with the lender. Lack of communication can lead to misunderstandings and unexpected outcomes.

Not retaining a copy of the completed form. After submission, individuals should keep a copy of the deed for their records. This can be important for future reference or if disputes arise.

Ignoring state-specific requirements. Each state may have unique rules regarding deeds in lieu of foreclosure. Individuals often overlook these requirements, which can complicate the process.

Filling out the Illinois Deed in Lieu of Foreclosure form can be a crucial step in managing your property situation. To help you navigate this process, here’s a list of things to do and avoid:

By following these guidelines, you can help ensure a smoother process when completing your Illinois Deed in Lieu of Foreclosure form.

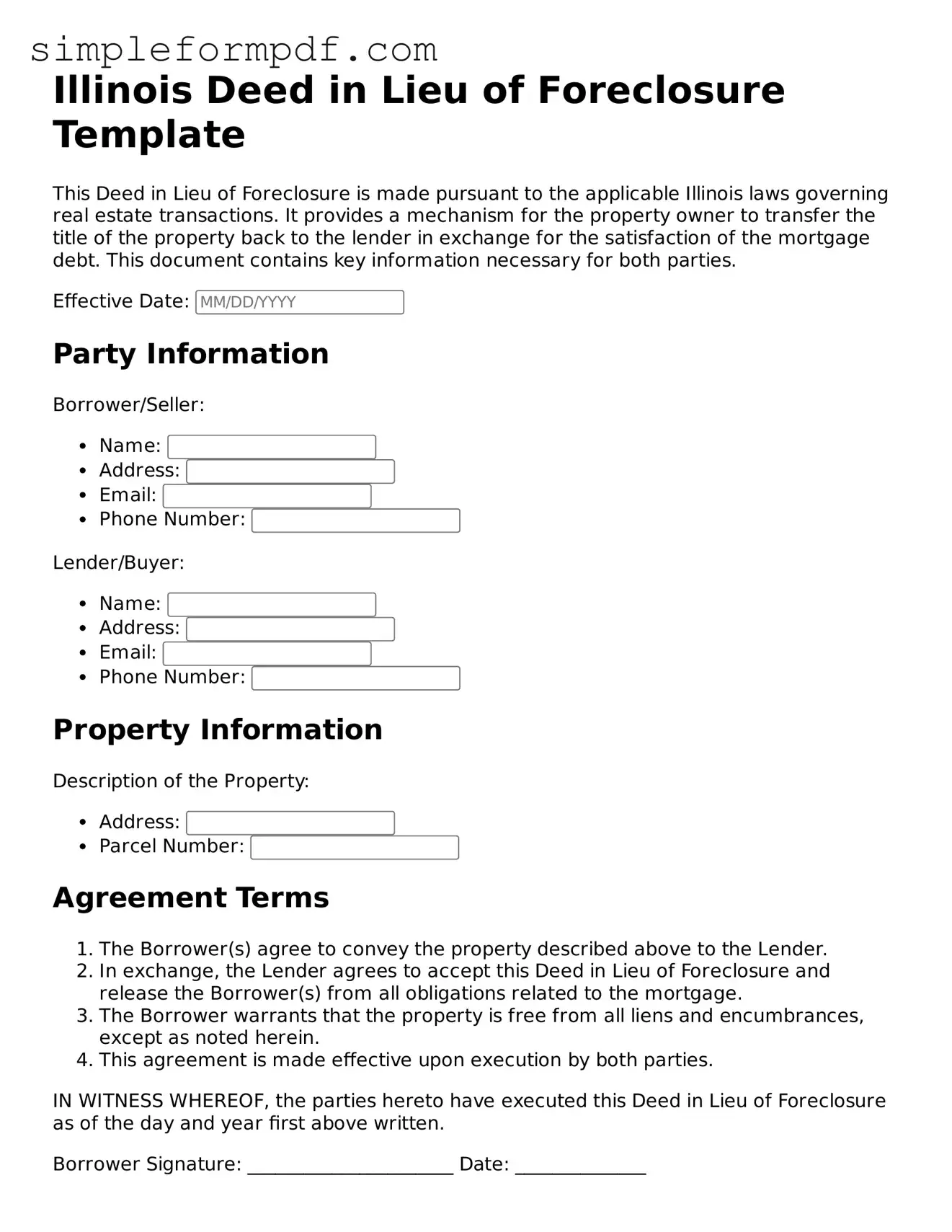

Illinois Deed in Lieu of Foreclosure Template

This Deed in Lieu of Foreclosure is made pursuant to the applicable Illinois laws governing real estate transactions. It provides a mechanism for the property owner to transfer the title of the property back to the lender in exchange for the satisfaction of the mortgage debt. This document contains key information necessary for both parties.

Effective Date:

Party Information

Borrower/Seller:

Lender/Buyer:

Property Information

Description of the Property:

Agreement Terms

IN WITNESS WHEREOF, the parties hereto have executed this Deed in Lieu of Foreclosure as of the day and year first above written.

Borrower Signature: ______________________ Date: ______________

Lender Signature: ______________________ Date: ______________

Witness Signature: ______________________ Date: ______________

Florida Deed in Lieu of Foreclosure - Homeowners should weigh all their options before proceeding with this form.

Deed in Lieu of Mortgage - It typically allows homeowners to mitigate the damage to their credit since it is less severe than foreclosure.

When embarking on the journey of homeschooling in Arizona, it is imperative for parents to understand the importance of the Arizona Homeschool Letter of Intent. This vital document not only serves as a formal declaration to the state but also ensures that families meet the necessary educational regulations. For detailed guidance on completing this process, visit azformsonline.com/homeschool-letter-of-intent to facilitate a smooth homeschooling experience.

California Pre-foreclosure Property Transfer - A Deed in Lieu often provides a clearer exit strategy in a tough housing market.

Deed in Lieu Vs Foreclosure - A deed in lieu might reduce the emotional toll associated with losing a home through foreclosure.

Understanding the Illinois Deed in Lieu of Foreclosure can be challenging, and several misconceptions often arise. Here are ten common misunderstandings about this legal process:

Many people believe that a deed in lieu of foreclosure wipes out all mortgage-related debts. However, it typically only addresses the mortgage itself. Other debts, such as second mortgages or liens, may still remain.

While a deed in lieu can be faster than a traditional foreclosure, it still requires paperwork and negotiations with the lender. It is not an instant solution.

A deed in lieu of foreclosure will likely impact your credit score negatively, though it may be less damaging than a full foreclosure.

Not all lenders are willing to accept a deed in lieu. Each lender has its own policies, and some may prefer to proceed with foreclosure.

While both options involve relinquishing property to avoid foreclosure, a short sale involves selling the property for less than what is owed, whereas a deed in lieu transfers ownership back to the lender without a sale.

A deed in lieu of foreclosure requires the lender's approval. You cannot simply decide to give the property back without their agreement.

While a deed in lieu transfers ownership, it may not relieve you of all liabilities. For example, if the property is in poor condition, you could still be held responsible for any damages or unpaid taxes.

Homeowners who are struggling to make payments but have not yet entered foreclosure can also pursue a deed in lieu as a proactive measure.

There is no guarantee that a lender will accept a deed in lieu of foreclosure. Approval depends on the lender's criteria and the homeowner's financial situation.

While signing a deed in lieu is a significant commitment, there may be options to negotiate or withdraw under certain circumstances before the transaction is finalized.

Understanding these misconceptions can help homeowners make informed decisions regarding their options when facing financial difficulties related to their property.

After completing the Illinois Deed in Lieu of Foreclosure form, you will need to submit it to the appropriate parties. This typically includes the lender and possibly the county clerk's office. Ensure that all required signatures are obtained and that the document is filed correctly to avoid any complications.