Free Promissory Note Form for the State of Florida

Free Promissory Note Form for the State of Florida

Not specifying the loan amount: One of the most common mistakes is failing to clearly state the amount being borrowed. This figure should be precise, as it forms the basis of the agreement.

Omitting interest rate details: If the loan involves interest, it's crucial to specify the rate. Leaving this out can lead to confusion and disputes later on.

Ignoring repayment terms: Clearly outline how and when payments will be made. Vague terms can create misunderstandings between the borrower and lender.

Not including a due date: Every promissory note should have a specific due date for repayment. Without it, the borrower might not feel urgency to repay the loan.

Failing to sign the document: A promissory note is not valid unless it is signed by the borrower. Forgetting this step can render the agreement unenforceable.

Not having a witness or notary: While not always required, having a witness or notary can add an extra layer of legitimacy to the document, which can be beneficial if disputes arise.

Using vague language: It's important to use clear and specific language throughout the note. Ambiguities can lead to different interpretations, which can complicate matters later.

Neglecting to include default provisions: What happens if the borrower fails to make payments? Including default provisions can protect the lender's interests.

Not keeping copies: After filling out the form, both parties should keep copies of the signed document. This ensures that everyone has access to the terms agreed upon.

A Promissory Note is a financial document that outlines a borrower's promise to repay a loan under specified terms. Several other documents share similarities with the Promissory Note, often serving related purposes in financial and legal transactions. Below are nine documents that are similar in nature:

When filling out the Florida Promissory Note form, it's important to follow certain guidelines to ensure accuracy and compliance. Here are some key dos and don'ts:

By following these guidelines, you can help ensure that your Promissory Note is properly executed and legally binding.

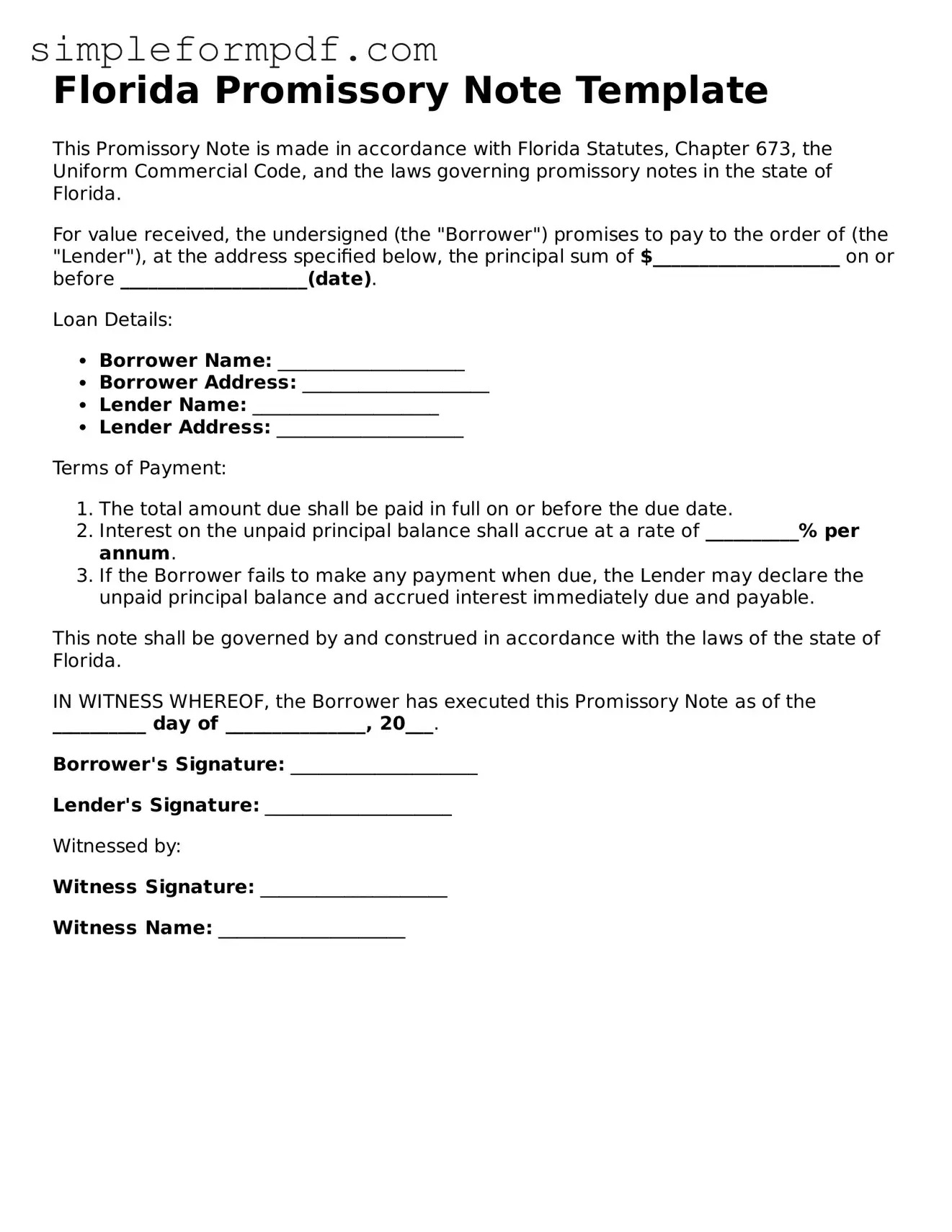

Florida Promissory Note Template

This Promissory Note is made in accordance with Florida Statutes, Chapter 673, the Uniform Commercial Code, and the laws governing promissory notes in the state of Florida.

For value received, the undersigned (the "Borrower") promises to pay to the order of (the "Lender"), at the address specified below, the principal sum of $____________________ on or before ____________________(date).

Loan Details:

Terms of Payment:

This note shall be governed by and construed in accordance with the laws of the state of Florida.

IN WITNESS WHEREOF, the Borrower has executed this Promissory Note as of the __________ day of _______________, 20___.

Borrower's Signature: ____________________

Lender's Signature: ____________________

Witnessed by:

Witness Signature: ____________________

Witness Name: ____________________

How to Create Promissory Note - Some promissory notes require collateral to secure the loan.

Promissory Note Texas - Promissory notes can involve personal relationships, like loans from family and friends, or formal business transactions.

Pennsylvania Promissory Note - A signed promissory note acts as a legal document, ensuring accountability for repayment.

A Non-disclosure Agreement (NDA) in Arizona is a legal contract designed to protect confidential information shared between parties. This form establishes the terms under which sensitive information must be kept private, preventing unauthorized disclosure. By signing an NDA, individuals and businesses can safeguard their proprietary knowledge and maintain a competitive edge, as outlined in the details found at https://azformsonline.com/non-disclosure-agreement/.

Promissory Note for Loan - The note may contain confidentiality clauses to protect sensitive information between parties.

Misconceptions about the Florida Promissory Note form can lead to misunderstandings regarding its use and enforceability. Below are five common misconceptions, along with clarifications for each.

All Promissory Notes Must Be Notarized. Many believe that notarization is a requirement for a promissory note to be valid in Florida. However, notarization is not mandatory. A promissory note can be legally binding without a notary's signature, provided it meets other essential criteria.

Promissory Notes Are Only Used for Real Estate Transactions. Some people think that promissory notes are exclusively for real estate deals. In reality, they can be used for various types of loans, including personal loans, business loans, and even informal agreements between friends or family members.

Interest Rates Must Be Specified in the Note. A common belief is that a promissory note must include a specified interest rate. While it is advisable to state the interest rate to avoid confusion, a note can still be valid even if it does not mention interest. In such cases, Florida law may apply a default interest rate.

Promissory Notes Are Not Enforceable in Court. Some individuals assume that promissory notes are informal and cannot be enforced legally. This is incorrect. A properly executed promissory note can be enforced in court, making it a powerful tool for lenders seeking repayment.

All Promissory Notes Are the Same. There is a misconception that all promissory notes follow a standard format. In fact, the terms and conditions can vary significantly. Each note should be tailored to the specific agreement between the parties involved, reflecting their unique circumstances and intentions.

After gathering the necessary information, you will be ready to fill out the Florida Promissory Note form. This document requires specific details to ensure clarity and legality. Follow these steps carefully to complete the form accurately.

Once the form is completed, keep a copy for your records and provide a copy to the other party. This ensures that both parties have access to the same information regarding the loan agreement.