Free Loan Agreement Form for the State of Florida

Free Loan Agreement Form for the State of Florida

Incomplete Information: One of the most common mistakes is failing to fill out all required fields. Each section must be completed to ensure the agreement is valid.

Incorrect Personal Details: Providing inaccurate personal information, such as your name or address, can lead to complications. Always double-check these details.

Not Understanding Loan Terms: Many people sign without fully understanding the loan terms. It's crucial to read and comprehend the interest rates, payment schedules, and any fees involved.

Missing Signatures: Forgetting to sign the agreement is a frequent oversight. Both parties must sign for the document to be legally binding.

Failing to Date the Agreement: Omitting the date can create confusion about when the agreement takes effect. Always include the date when signing.

Not Keeping a Copy: After filling out the form, some individuals forget to keep a copy for their records. Retaining a copy is essential for future reference.

Ignoring State Regulations: Each state has specific laws regarding loan agreements. Failing to comply with Florida's regulations can render the agreement unenforceable.

Overlooking Additional Terms: Some people skip over additional clauses or terms that may be included. These can significantly impact the loan, so they should not be ignored.

Promissory Note: A promissory note is a written promise to pay a specified amount of money at a designated time. Like a loan agreement, it outlines the borrower's obligation to repay the loan, including interest rates and repayment terms.

Mortgage Agreement: This document secures a loan with real property. It details the borrower's promise to repay the loan and grants the lender the right to take possession of the property if the borrower defaults.

Security Agreement: A security agreement outlines the terms under which collateral is pledged to secure a loan. Similar to a loan agreement, it specifies the borrower's obligations and the lender's rights in case of default.

Lease Agreement: A lease agreement allows one party to use another's property in exchange for payment. It includes terms similar to those in a loan agreement, such as duration, payment amounts, and conditions for default.

Line of Credit Agreement: This document provides a borrower access to a specified amount of credit. It shares similarities with a loan agreement in detailing repayment terms and interest rates, but it allows for more flexible borrowing.

Installment Sale Agreement: An installment sale agreement allows a buyer to purchase an asset over time through scheduled payments. It includes terms regarding payment amounts and timelines, akin to those in a loan agreement.

Credit Card Agreement: This agreement outlines the terms under which a credit card is issued. It specifies the borrower's obligations to repay borrowed amounts, interest rates, and fees, similar to a loan agreement.

Personal Loan Agreement: A personal loan agreement details the terms of a loan made to an individual. It includes repayment schedules, interest rates, and conditions for default, mirroring the structure of a standard loan agreement.

Business Loan Agreement: This document is specifically for loans made to businesses. It outlines the terms of repayment, interest rates, and collateral, similar to personal loan agreements but tailored for business needs.

Debt Settlement Agreement: A debt settlement agreement outlines the terms under which a debtor agrees to pay a reduced amount to settle a debt. It shares similarities with a loan agreement in terms of outlining obligations and consequences of default.

When filling out the Florida Loan Agreement form, there are important guidelines to follow to ensure accuracy and compliance. Here’s a helpful list of what to do and what to avoid:

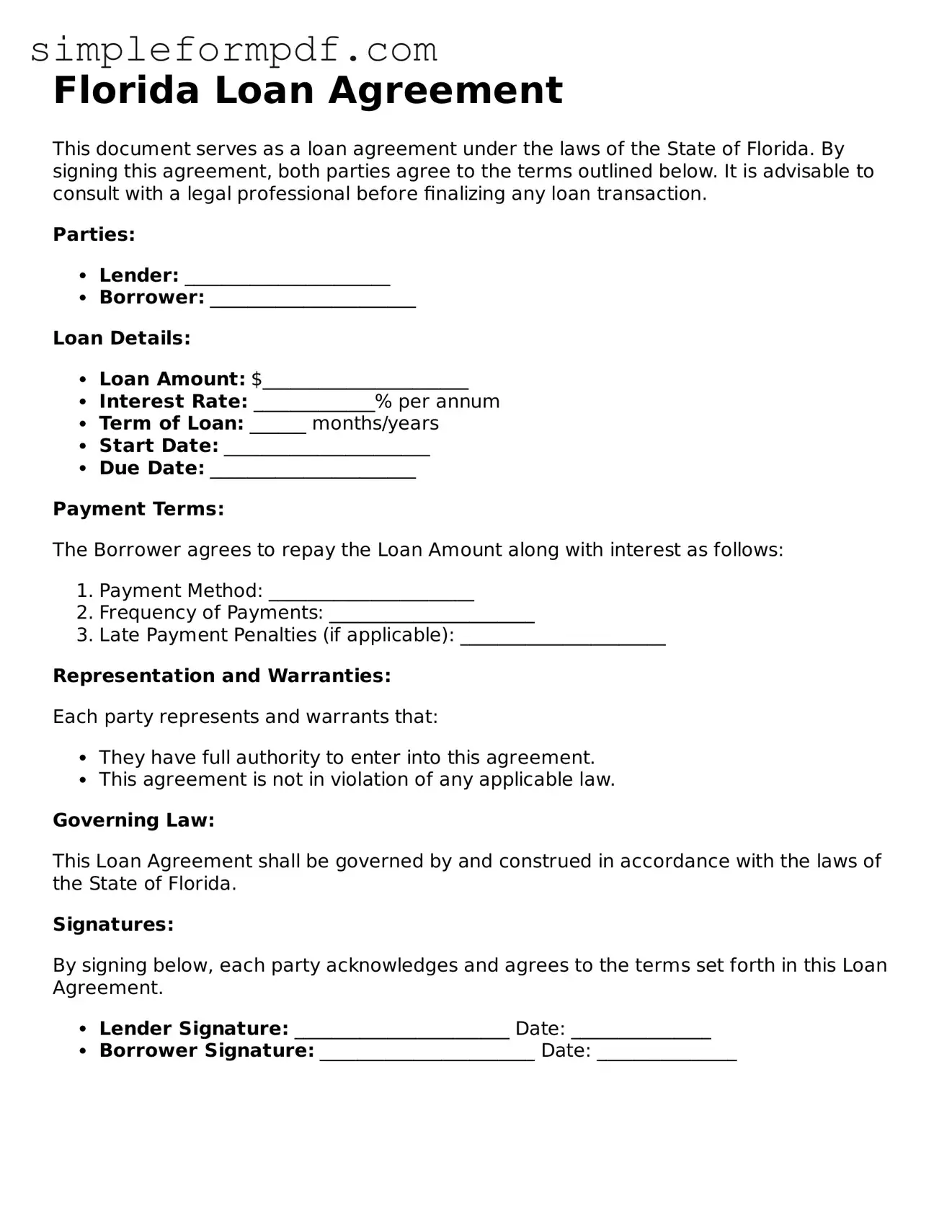

Florida Loan Agreement

This document serves as a loan agreement under the laws of the State of Florida. By signing this agreement, both parties agree to the terms outlined below. It is advisable to consult with a legal professional before finalizing any loan transaction.

Parties:

Loan Details:

Payment Terms:

The Borrower agrees to repay the Loan Amount along with interest as follows:

Representation and Warranties:

Each party represents and warrants that:

Governing Law:

This Loan Agreement shall be governed by and construed in accordance with the laws of the State of Florida.

Signatures:

By signing below, each party acknowledges and agrees to the terms set forth in this Loan Agreement.

Illinois Promissory Note - The agreement can include provisions for early repayment options.

For those looking to purchase or sell a trailer in Missouri, it is crucial to have a properly completed Missouri Trailer Bill of Sale form, which can be found at Missouri PDF Forms. This document not only legitimizes the transaction but also ensures all necessary information is documented to avoid future disputes.

Free Promissory Note Template Texas - Provides for confidentiality obligations concerning the agreement.

Understanding the Florida Loan Agreement form is essential for borrowers and lenders alike. However, several misconceptions can lead to confusion. Here are ten common misconceptions explained:

Being aware of these misconceptions can help individuals navigate the loan process more effectively and ensure that their rights are protected.

Filling out the Florida Loan Agreement form is a straightforward process. After completing the form, you will be prepared to formalize your loan arrangement. Make sure to review your entries for accuracy before submitting the document.