Free Deed in Lieu of Foreclosure Form for the State of California

Free Deed in Lieu of Foreclosure Form for the State of California

Incomplete Information: Failing to provide all necessary details can lead to delays or rejection. Ensure that all sections are filled out accurately.

Incorrect Property Description: Misidentifying the property can cause legal complications. Double-check the property address and legal description.

Not Notarizing the Document: A deed in lieu of foreclosure must be notarized to be legally binding. Omitting this step can invalidate the document.

Failure to Review Lender Requirements: Each lender may have specific requirements. Ignoring these can result in rejection of the deed.

Not Understanding Tax Implications: People often overlook potential tax consequences. Consulting a tax advisor can provide clarity on this matter.

Ignoring Other Liens: If there are other liens on the property, they must be addressed. A deed in lieu does not automatically eliminate these obligations.

Not Keeping Copies: Failing to retain copies of the completed form can lead to issues in the future. Always keep a copy for your records.

Assuming Immediate Release of Liability: A deed in lieu does not always guarantee immediate release from the mortgage obligation. Clarify this with the lender.

Neglecting to Seek Legal Advice: Many individuals do not consult a legal professional. Doing so can help avoid costly mistakes and ensure compliance with all legal requirements.

When filling out the California Deed in Lieu of Foreclosure form, it's essential to approach the process with care. Here are some important dos and don'ts to consider:

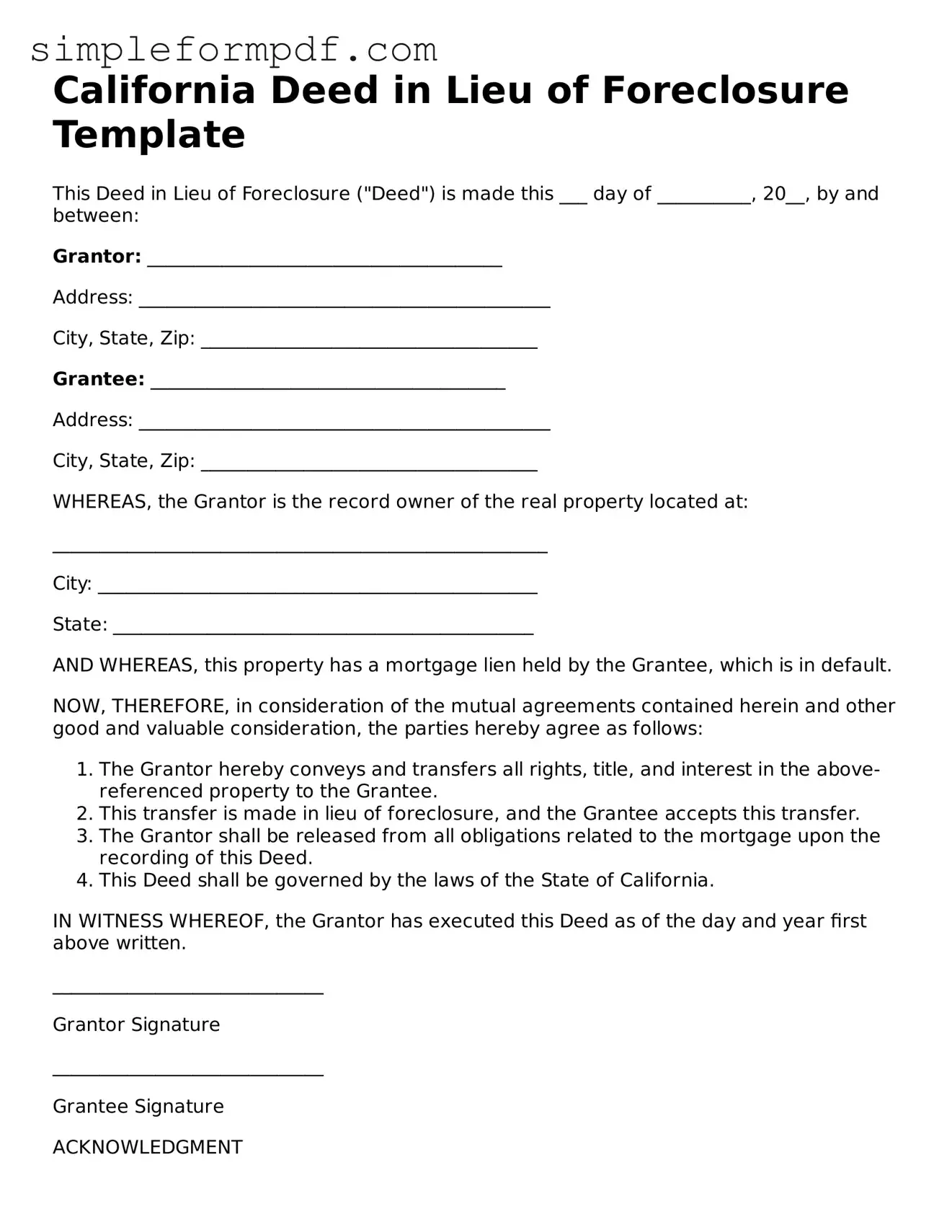

California Deed in Lieu of Foreclosure Template

This Deed in Lieu of Foreclosure ("Deed") is made this ___ day of __________, 20__, by and between:

Grantor: ______________________________________

Address: ____________________________________________

City, State, Zip: ____________________________________

Grantee: ______________________________________

Address: ____________________________________________

City, State, Zip: ____________________________________

WHEREAS, the Grantor is the record owner of the real property located at:

_____________________________________________________

City: _______________________________________________

State: _____________________________________________

AND WHEREAS, this property has a mortgage lien held by the Grantee, which is in default.

NOW, THEREFORE, in consideration of the mutual agreements contained herein and other good and valuable consideration, the parties hereby agree as follows:

IN WITNESS WHEREOF, the Grantor has executed this Deed as of the day and year first above written.

_____________________________

Grantor Signature

_____________________________

Grantee Signature

ACKNOWLEDGMENT

State of California

County of __________

On this ___ day of __________, 20__, before me, _______________ (Notary Public), personally appeared __________________ (Grantor's Name) and __________________ (Grantee's Name), who proved to me on the basis of satisfactory evidence to be the persons whose names are subscribed to the within instrument and acknowledged to me that they executed the same in their authorized capacities.

WITNESS my hand and official seal.

_____________________________

Notary Public Signature

Deed in Lieu Vs Foreclosure - The deed in lieu of foreclosure can offer a cleaner exit from home ownership challenges.

The Arizona Durable Power of Attorney form, available at https://azformsonline.com/durable-power-of-attorney, is a vital legal document that empowers an individual to appoint someone else to make crucial decisions on their behalf in financial and legal matters, remaining valid even in cases of incapacitation, and ensuring that their personal and financial interests are safeguarded.

Deed in Lieu of Foreclosure Florida - Taking this route may also allow the homeowner to negotiate better terms with the lender.

Many homeowners facing financial difficulties may consider a Deed in Lieu of Foreclosure in California. However, there are several misconceptions about this process. Below is a list of ten common misunderstandings.

Understanding these misconceptions can help homeowners make informed decisions regarding their financial options.

After completing the California Deed in Lieu of Foreclosure form, you will need to submit it to your lender. This step is crucial, as it allows the lender to process your request. Be sure to keep copies of everything for your records.